An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

In the latter half of the 19th century, Pennsylvania dominated the U.S. oil market. The first oil well was drilled in Titusville, Pennsylvania, in 1859, prompting the first oil boom in the United States. Pennsylvania was the leading U.S. producer of oil until the 1901 Texas oil boom.1 With the recent drilling in the Marcellus Shale—the largest shale formation in the United States, spanning six northeastern states—the growth in shale gas production in Pennsylvania has revived the state’s important role in the nation’s oil and natural gas industry. This article presents employment and wage trends in Pennsylvania’s oil and natural gas industry over the 2007–2012 period. It also compares that industry with the state’s economically important coal mining industry.

The U.S. Energy Information Administration (EIA) projects that U.S. annual natural gas production will increase from 23.0 trillion cubic feet in 2011 to 33.1 trillion cubic feet in 2040, a gain of 10.1 trillion cubic feet (44.0 percent).2 More than 87 percent of this increase is due to growth in shale gas production, whose share of total natural gas production is projected to reach 50.4 percent by 2040.3 Because of this rapid growth, the oil and natural gas industry has experienced large employment and wage increases over the past few years. Many of these increases have occurred in areas outside the “oil patch” region, which produces a substantial amount of U.S. oil and natural gas and comprises the states of Oklahoma, Texas, and Louisiana. (For states whose employment in the oil and natural gas industry changed by more than 1,000 over the 2007–2012 period, see figure 1.)

Shale gas is natural gas trapped within shale formations, which are made of thin layers of fine-grained sedimentary rocks. These shale formations cover a wide area. Conventional vertical wells can only access a small vertical layer of shale, making the extraction of gas deposits uneconomical. Horizontal drilling, that is, drilling along the thin layers of rock, has allowed gas producers to access much more natural gas from shale deposits. Gas producers have effectively used horizontal drilling with hydraulic fracturing (commonly called fracking), which is an extraction technique in which water, chemicals, and sand are pumped into the horizontal wells to fracture the shale rock and allow natural gas to flow out. These two techniques, when used in combination, have enabled gas producers to extract shale gas both rapidly and economically.

The nation’s most developed shale “play” (i.e., a commercially exploited geographical area or energy deposit) is the Barnett Shale in Texas, where drilling began in the late 1990s. Since 2003, the use of horizontal wells in the Barnett Shale has increased considerably.4 Strong economic results from this practice have led to drilling in other areas, such as the Haynesville and Fayetteville shale plays in Texas, Louisiana, and Arkansas.

However, the most interesting shale development is in the Marcellus Shale. Much of the recent drilling in that shale has occurred in Pennsylvania, a traditionally coal-producing state that has seen a surge in natural gas production and employment over the past few years. Counties in northeastern and southwestern Pennsylvania have been most affected by the growth in natural gas production.

This article uses annual data from the Bureau of Labor Statistics Quarterly Census of Employment and Wages (QCEW) program for the period 2007–2012. Data from 2007 present Pennsylvania’s oil and natural gas industry before the expanded use of horizontal drilling in the state,5 whereas data from 2012 are the most recent annual data available from QCEW.

For the purposes of this article, the oil and natural gas industry is defined as an aggregate of three industries: (1) oil and gas extraction (North American Industry Classification System (NAICS) 211), which represents establishments that operate and develop oil and gas fields; (2) drilling oil and gas wells (NAICS 213111), which contains establishments that drill oil and gas wells, as well as contractors that specialize in directional drilling; and (3) support activities for oil and gas operations (NAICS 213112), which comprises establishments that perform support activities, such as exploring, building, and dismantling wells. The coal mining industry is defined as an aggregate of two industries: coal mining (NAICS 21211) and support activities for coal mining (NAICS 213113). Establishments in these industries are primarily engaged in support activities, such as exploring, blasting, and tunneling, as well as the actual mining of coal.

From 2007 to 2012, the total annual average employment in all U.S. industries decreased by 3.7 million (

| Industry | Employment | Average annual pay | ||

|---|---|---|---|---|

| Level change | Percent change | Level change | Percent change | |

United States, all industries | –3,669,728 | –2.7 | $4,831 | 10.9 |

Oil and natural gas industry | 135,084 | 31.6 | 13,624 | 14.6 |

Oil and gas extraction (NAICS 211) | 41,922 | 28.7 | 22,552 | 17.0 |

Drilling oil and gas wells (NAICS 213111) | 7,815 | 9.2 | 12,017 | 15.0 |

Support activities for oil and gas operations (NAICS 213112) | 85,347 | 43.3 | 9,789 | 13.9 |

Coal mining industry | 10,962 | 13.0 | 11,693 | 17.3 |

Coal mining (NAICS 21211) | 9,321 | 12.2 | 11,588 | 16.8 |

Support activities for coal mining (NAICS 213113) | 1,641 | 21.8 | 13,821 | 26.1 |

| Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages program. | ||||

Average annual pay grew by a larger amount in the oil and natural gas industry than it did in the national economy.6 From 2007 to 2012, the U.S. average annual pay increased by $4,831 (10.9 percent), to $49,289. Over the same period, workers in the oil and natural gas industry saw, on average, an annual pay increase of $13,624 (14.6 percent). In 2012, the average annual pay in that industry was $107,198, which is $57,909 higher than the average annual pay across all industries.

Between 2007 and 2012, employment grew in each of the three oil- and natural gas-related industries. The absolute and percent growth in the average annual pay of these industries also was larger than the growth in national average annual pay. Support activities for oil and gas operations had the largest increase in employment over the study period, adding 85,347 jobs (an increase of 43.3 percent) and reaching a 2012 level of 282,447 jobs, the largest employment level among the three industries. Oil and gas extraction had the largest pay increase, $22,552 (17.0 percent), and, by the end of the period, the largest annual pay, $155,062.

In terms of employment, the oil and natural gas industry is substantially larger than the coal mining industry. In 2012, the oil and natural gas industry had nearly six times the number of jobs the coal mining industry had. Furthermore, over the 2007–2012 period, the oil and natural gas industry added more jobs than did the coal mining industry. From 2007 to 2012, employment in the coal mining industry increased by 10,962 (13.0 percent), from 84,131 in 2007 to 95,093 in 2012. By comparison, over the same period, employment in the oil and natural gas industry grew by 135,084 (31.6 percent), from 427,706 in 2007 to 562,790 in 2012. (See table 1.)

Although employment in the oil and natural gas industry is larger, employment in the coal mining industry is more stable. (See figure 2.) Compared with the coal mining industry, the oil and natural gas industry experienced larger percent changes in employment in each year over the 2007−2012 period. The oil and natural gas industry also was more sensitive to the steep economic downturn of the Great Recession, seeing a sharp over-the-year decrease in employment growth, from 11.4 percent in 2008 to −11.4 percent in 2009. While the rate of employment growth in the coal mining industry did fall from 2008 to 2009, the percent change in employment was notably smaller, dropping from 6.0 percent in 2008 to 0.9 percent in 2009, and falling further, to −0.8 percent, in 2010. By 2011, both industries had recovered from recession lows, reaching rates of employment growth comparable to those in 2008.

Further, since 2007, average annual pay in the oil and natural gas industry has been consistently greater than the pay in the coal mining industry. In 2012, average annual pay in the oil and natural gas industry was $107,198, compared with $79,127 in the coal mining industry. Moreover, from 2007 to 2012, pay grew by a larger amount in the oil and natural gas industry than it did in the coal mining industry, although coal mining experienced a slightly larger percent increase over the 5-year period. While the average annual pay in the oil and natural gas industry gained $13,624 (14.6 percent), pay in coal mining gained $11,693 (17.3 percent).

Table 2 shows the top 10 states ranked by employment in the oil and natural gas industry. The ranking is presented (1) by employment level in 2007, (2) by employment level in 2012, and (3) by employment change from 2007 to 2012. Nine states that were in the top 10 in 2007 also were in the top 10 in 2012. Many of these states are traditionally oil- and gas-producing states, as indicated by their high employment levels and relatively small employment changes in the industry over the study period. North Dakota is the only new state ranked in the top 10 in 2012; however, its large employment increase can be attributed to the growth in shale oil production in the Bakken Shale and does not represent a substantial increase in natural gas employment.7

| Annual average employment 2007 | Average annual employment 2012 | Increase in annual average employment 2007–2012 | ||||

|---|---|---|---|---|---|---|

| State | Level | State | Level | State | Level change | Percent change |

Texas | 194,818 | Texas | 259,333 | Texas | 64,515 | 33.1 |

Louisiana | 46,624 | Oklahoma | 56,040 | Pennsylvania | 15,114 | 259.3 |

Oklahoma | 44,005 | Louisiana | 50,695 | North Dakota(1) | 12,477 | 354.3 |

Colorado | 18,908 | Colorado | 24,043 | Oklahoma | 12,035 | 27.3 |

California | 18,431 | California | 22,661 | Colorado | 5,135 | 27.2 |

Wyoming | 17,743 | Pennsylvania | 20,943 | California | 4,230 | 23.0 |

New Mexico | 15,093 | New Mexico | 18,560 | Louisiana | 4,071 | 8.7 |

Alaska | 11,651 | Wyoming | 17,121 | New Mexico | 3,467 | 23.0 |

Kansas | 8,065 | North Dakota(1) | 15,999 | Alaska | 1,990 | 17.1 |

Pennsylvania | 5,829 | Alaska | 13,641 | Arkansas | 1,897 | 40.5 |

Notes: (1) North Dakota's 2012 employment in the oil and natural gas industry is an incomplete sum. Data for the drilling oil and gas well industry (NAICS 213111) are not disclosable. The state's employment level and over-the-period increase in employment may be understated because they are calculated on the basis of an incomplete sum. Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages program. | ||||||

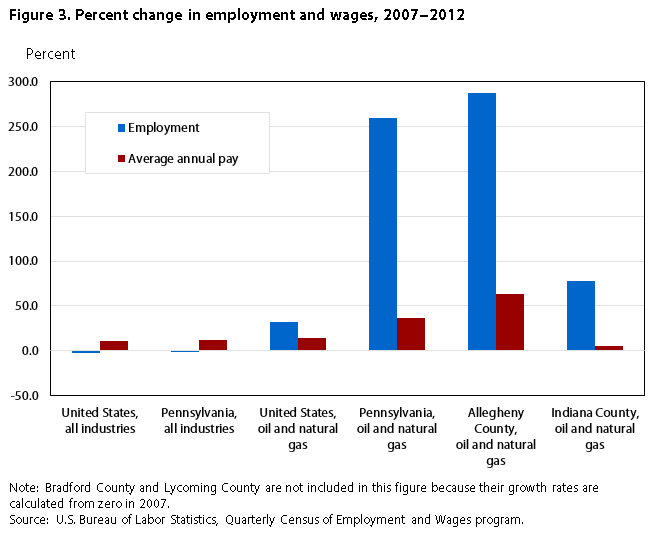

Most of Pennsylvania’s substantial employment gains in the oil and natural gas industry were due to the recent surge in shale gas production brought about by the drilling in the Marcellus Shale. The state’s employment growth in the industry is consistent with EIA data on gross withdrawals from shale gas wells. Pennsylvania had the second-highest increase in gross withdrawals (2.0 trillion cubic feet) from 2008 to 2012, trailing only Louisiana in this regard.8 As a result, Pennsylvania went from being the 10th-largest state by oil and natural gas employment in 2007 to being the 6th largest in 2012. The state also had the second-largest employment increase over the study period, positioning itself only after Texas, a major oil- and natural gas-producing state.

Despite recent declines in Pennsylvania’s overall economy, the state’s oil and natural gas industry has seen substantial growth in terms of both employment and wages. (See figure 3.) From 2007 to 2012, total annual average employment in Pennsylvania declined by 74,133 (–1.3 percent), to 5,578,414; by contrast, employment in the oil and natural gas industry increased by 15,114 (259.3 percent) over the same period. In addition, while the state’s average annual pay increased by $5,158 (11.9 percent), to $48,397 in 2012, wages in Pennsylvania’s oil and natural gas industry rose by $22,104 (36.3 percent), to $82,974 in 2012.

Pennsylvania is part of the Appalachian coal region.9 All anthracite coal mines in the United States are found in northeastern Pennsylvania,10 and the state's bituminous coal mines are mostly found in western Pennsylvania.11 In 2012, the state ranked fourth in terms of coal production; it produced 54.7 million short tons of coal, representing 5.4 percent of total U.S. coal production.12

Pennsylvania has a higher-than-average concentration of employment in the coal mining industry. Employment concentrations across industries and geographic areas are compared with the use of ratios called location quotients.13 In 2007, Pennsylvania had a location quotient of 2.36 for the coal mining industry, meaning that the state had nearly 2.4 times as many jobs in that industry (as a percentage of total state employment) as did the United States overall. Most notably, the location quotient for the anthracite coal mining industry (NAICS 212113) was 18.43. In 2012, Pennsylvania’s location quotient for the coal mining industry was the same as that in 2007.

The location quotient for Pennsylvania’s oil and natural gas industry was only 0.33 in 2007. By 2012, however, that quotient was 0.88, which is more than two-and-a-half times the value seen in 2007. Pennsylvania now has nearly the same concentration of employment in the oil and natural gas industry as that for the United States overall. Although the state’s employment is less concentrated in the oil and natural gas industry than it is in the coal mining industry—a difference explained by more evenly distributed oil and gas deposits across states—Pennsylvania’s oil and natural gas industry has experienced substantial employment growth, higher than that seen in the coal mining industry. By 2012, the state’s oil and natural gas industry had achieved not only higher employment but also higher average annual pay than the coal mining industry. (See figures 4 and 5.)

In 2007, before the expansion of shale gas production, employment in Pennsylvania’s coal mining industry was larger than employment in the state’s oil and natural gas industry. However, the same was not true at the level of the national economy, where, from 2007 to 2012, the oil and natural gas industry was consistently larger than the coal mining industry. Within Pennsylvania, there were 8,276 jobs in the coal mining industry in 2007, compared with 5,829 jobs in the oil and natural gas industry in that year. Over the study period, employment in the coal mining industry increased by 1,244 (15.0 percent), to 9,520 in 2012. However, employment in the oil and natural gas industry had reached a level of 20,943 by the end of the period, surpassing employment in the coal mining industry.

Moreover, from 2007 to 2012, the increase in average annual pay in Pennsylvania’s oil and natural gas industry was greater than the corresponding increase in the state’s coal mining industry. Over the study period, annual average pay in the coal mining industry grew by $14,184, from $63,201 in 2007 to $77,385 in 2012. Although the pay in the oil and natural gas industry was lower at the start of the period, by 2012, it had reached a level of $82,974, which is $5,589 higher than the 2012 pay level in the coal mining industry. Both industries had higher annual pay than the overall Pennsylvania average, which was $48,397 in 2012.

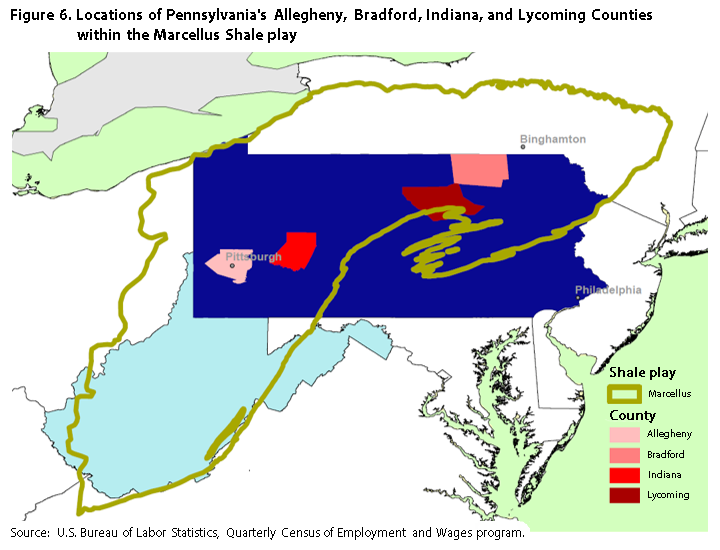

According to the EIA, the largest increase in Pennsylvania’s natural gas production occurred in northeastern Pennsylvania, although a smaller increase also occurred in southwestern Pennsylvania.14 In addition, QCEW data show strong employment growth in the oil and natural gas industry in these regions. (For locations of Pennsylvania counties with large growth in natural gas production and employment, see figure 6.)

In northeastern Pennsylvania, Lycoming County had zero reported jobs in the oil and natural gas industry in 2007. By 2012, employment in the county had grown to 1,801, the second-highest level among all counties in the state. From 2007 to 2012, Lycoming also experienced the largest gain15 in oil and natural gas employment. Similarly, while Bradford County had zero employment in the oil and natural gas industry in 2007, its employment had grown to 983 by 2012.16

Average annual pay in the oil and natural gas industry in Lycoming and Bradford Counties also was relatively high compared with that in other counties in the state. In 2012, Lycoming had an average annual pay of $75,860, the seventh-highest pay among all Pennsylvania counties in that year. Also in 2012, Bradford had the third-highest average annual pay in the state’s oil and natural gas industry, at $86,840.

In southwestern Pennsylvania, Allegheny County, where Pittsburgh is located, had the largest increase in oil and natural gas employment in the region from 2007 to 2012. Employment in this county increased by 1,283 (287.0 percent), to reach a level of 1,730 in 2012.17 Among all Pennsylvania counties, Allegheny experienced the second-largest employment gain in the oil and natural gas industry from 2007 to 2012. Over the same period, the county’s average annual pay in that industry increased by $55,343 (63.7 percent), to $142,222, which was the highest pay among all counties in Pennsylvania in 2012.

Also within the southwestern Pennsylvania region, Indiana County experienced a significant increase in oil and natural gas employment, adding 1,051 jobs (an increase of 78.3 percent) from 2007 to 2012. Indiana County had the highest level of employment in the oil and natural gas industry among all counties, both in 2007, when employment was 1,343, and in 2012, when employment was 2,394. In 2007, Indiana County’s oil and natural gas industry also had a comparatively high average annual pay, $63,427, which was the third highest among all Pennsylvania counties. However, from 2007 to 2012, pay saw a relatively small increase of $3,553 (5.6 percent), dropping Indiana County to 10th place in terms of oil and natural gas industry pay.

DESPITE A LARGE EMPLOYMENT DECREASE during the Great Recession, and in contrast to the decline in overall national employment over the study period, the U.S. oil and natural gas industry grew from 2007 to 2012. Advancements in horizontal drilling and hydraulic fracturing have allowed rapid growth in shale gas production in many shale plays across the United States. The recent development in the Marcellus Shale is especially interesting because the formation spans a large area of the Northeast, a region not historically known for natural gas production. Pennsylvania’s oil and natural gas industry is now larger than the coal mining industry for which the state is traditionally known.

Jennifer Cruz, Peter W. Smith, and Sara Stanley, "The Marcellus Shale gas boom in Pennsylvania: employment and wage trends," Monthly Labor Review, U.S. Bureau of Labor Statistics, February 2014, https://doi.org/10.21916/mlr.2014.7

1 “The world of oil: the history of Titusville, PA” (Ithaca, NY: Paleontological Research Institution and its Museum of the Earth; and Cayuga Nature Center).

2 “Annual energy outlook 2013,” table 13 (U.S. Energy Information Administration, April 2013), http://www.eia.gov/forecasts/aeo/MT_naturalgas.cfm.

3 “Annual energy outlook 2013,” figure 91 (U.S. Energy Information Administration, April 2013), http://www.eia.gov/forecasts/aeo/MT_naturalgas.cfm.

4 “Technology drives natural gas production growth from shale gas formations” (U.S. Energy Information Administration, July 2011), http://www.eia.gov/todayinenergy/detail.cfm?id=2170.

5 “Horizontal drilling boosts Pennsylvania’s natural gas production” (U.S. Energy Information Administration, May 2012), http://www.eia.gov/todayinenergy/detail.cfm?id=6390.

6 For the aggregate oil and natural gas industry and the aggregate coal mining industry, average annual pay was calculated by dividing the sum of total annual wages by the sum of annual average employment.

7 “North Dakota crude oil production continues to rise” (U.S. Energy Information Administration, August 2012), http://www.eia.gov/todayinenergy/detail.cfm?id=7550.

8 “Natural gas summary,” data series: gross withdrawals from shale gas wells (U.S. Energy Information Administration, January 2014), http://www.eia.gov/dnav/ng/ng_sum_lsum_a_EPG0_FGS_mmcf_a.htm. There were no 2007 data for gross withdrawals from shale gas wells for Pennsylvania. Data are available for 2008, when the shift to horizontal drilling began.

9 “Coal explained: where our coal comes from” (U.S. Energy Information Administration, July 2012), http://www.eia.gov/energyexplained/index.cfm?page=coal_where.

10 “Subbituminous and bituminous coal dominate U.S. coal production” (U.S. Energy Information Administration, August 2011), http://www.eia.gov/todayinenergy/detail.cfm?id=2670. See also “Annual coal report,” table 6 (U.S. Energy Information Administration, November 2012), http://www.eia.gov/coal/annual/. Anthracite coal is hard coal of the highest quality in terms of carbon count, purity, and heat content. By contrast, bituminous coal is relatively soft, with purity and energy content lower than those of anthracite coal but higher than those of the lowest graded lignite coal.

11 “Map 11: Distribution of Pennsylvania coals,” third ed. (Pennsylvania Department of Conservation and Natural Resources, 2000), http://www.dcnr.state.pa.us/cs/groups/public/documents/document/dcnr_008139.pdf.

12 “Annual coal report,” table 1 (U.S. Energy Information Administration, November 2012), http://www.eia.gov/coal/annual/.

13 Location quotients are ratios that compare a local area’s distribution of employment, by industry, to the national distribution (the base area). Location quotients are calculated by taking a local area’s employment within an industry as a percentage of total local area employment and dividing it by the industry’s national employment as a percentage of total national employment. A location quotient greater than 1.0 indicates an industry with a greater share of local area employment than of national employment. Conversely, an industry with a location quotient less than 1.0 has a lower share of local area employment than of national employment. The QCEW location quotient calculator is available online at https://data.bls.gov/location_quotient/ControllerServlet.

14 “Pennsylvania drives Northeast natural gas production growth” (U.S. Energy Information Administration, August 2011), http://www.eia.gov/todayinenergy/detail.cfm?id=2870.

15 The QCEW program has a county-level employment designation known as “unknown or undefined,” which is used in cases where employment cannot be reported in a single county. Some employers do not report data for each of their locations in the state, but instead report only their state totals. These employers are counted in the “unknown or undefined” category. Although this county designation had the largest employment increase from 2007 to 2012 and the highest 2012 level of employment in the oil and natural gas industry, it is not discussed in the article because it represents employment that is spread out among many counties.

16 Bradford County’s 2012 employment in the oil and natural gas industry is an incomplete sum. Data for the oil and gas extraction industry (NAICS 211) are not disclosable. The county’s employment level and over-the-period increase in employment may be understated because they are calculated on the basis of an incomplete sum.

17 Allegheny County’s 2007 employment in the oil and natural gas industry is an incomplete sum. Data for the drilling oil and gas wells industry (NAICS 213111) are not disclosable. The county’s over-the-period increase in employment may be understated because it is calculated on the basis of an incomplete sum.