An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

Nonfarm payroll employment in the United States continued to grow in 2014, according to data from the Current Employment Statistics (CES) survey.1 The economy added a total of 3.1 million jobs—the largest annual gain since 1999 and an average monthly employment increase of 260,000. Marking a milestone in 2014, both total private and total nonfarm employment recovered from the severe effects of the most recent (2007–2009) recession. (See figure 1.) Total private employment recovered in February 2014 and total nonfarm employment recovered 2 months later. (See figure 2.) Their recovery periods—74 months and 75 months, respectively—were the most protracted in the history of CES payroll employment. By the end of 2014, however, half of industry groups that suffered job losses during the most recent employment downturn had completely recovered from these losses and employment was expanding beyond the previous peak level. The other half, despite not recovering all jobs lost, did see job growth pick up in 2014.

In addition to employment, several other CES data series tell a positive story for 2014. Average weekly hours of all employees increased by 0.3 hour (or 0.9 percent), to 34.6 hours, marking the largest annual percent gain in hours since 2010. For all employees, the over-the-year growth in average hourly earnings was $0.44, about the same as in 2013. However, coupled with the increase in weekly hours, this gain resulted in average weekly earnings of $851.85, a gain of $22.48, or 2.7 percent. This percent increase is the largest annual increase since 2010. Real, or inflation-adjusted, average weekly earnings of all employees rose by 2.0 percent, the largest 12-month gain in weekly earnings since 2008. This gain indicates that although earnings increases may not be especially large, they are outpacing inflation.

Finally, the 12-month diffusion index of employment change shows that employment growth was spread broadly across component industries. This index, in which a value above 50 indicates a greater number of job-gaining than job-losing industries over 12 months, remained above 70.0 throughout 2014 and ended the year at 77.9, the highest level since 1997. Employment changes in recovered industries, in recovering industries, and in education and health services (in which employment grew throughout the most recent recession) are discussed in detail below. (See figure 2.)

Job growth in leisure and hospitality continued to be robust in 2014. This industry, which experienced a relatively shallow and brief recessionary job loss, had recovered by January 2012 and had added more than triple the number of jobs lost by the end of 2014. Over the year, the industry added 482,000 workers to payrolls, only slightly less than the 485,000 workers added in 2013. As in previous years, growth was concentrated in the food services and drinking places industry, which added 401,000 jobs in 2014.

The main contributor to employment gains within food services and drinking places was the restaurants and other eating places industry.2 Within this industry, both full-service and limited-service restaurants continued to show strength, adding 164,000 and 145,000 jobs, respectively, in 2014. Employment in food services and drinking places ended the year 13 percent above its most recent (December 2007) peak. In December 2014, this industry accounted for 73 percent of employment within leisure and hospitality.

The leisure and hospitality industry is largely dependent on families’ disposable income, and it is among the first to benefit or suffer from changes in that income.3 This industry has continued to show strength on the backdrop of recent consumer optimism about the nation’s economic outlook. The Consumer Confidence Index,4 a measure and economic indicator of consumer confidence, can be volatile, but has remained on an upward trend since mid-2009 (see figure 3). With the recent decline in gas prices, consumers have had more disposable income, a change that has most likely contributed to increases seen in same-store traffic and in food sales.5 Despite fluctuations in the Consumer Confidence Index, employment within leisure and hospitality has continued its trend of growth, with food services and drinking places employment paving the way.

Mining and logging has also seen a period of sustained job expansion since June 2011. By the end of 2014, the industry had added more than double the jobs lost during the recession. Over the year, employment grew by 42,000, an annual increase of 4.8 percent, well above the increases experienced in 2012 (2.4 percent) and in 2013 (2.2 percent). Employment growth in 2014 was concentrated in the oil and gas components of mining, with the largest gain occurring in support activities for oil and gas operations, which added 27,000 jobs over the year. Job growth in oil and gas industries is likely due to increased U.S. oil and gas production. Improved extraction technologies, such as horizontal drilling and hydraulic fracturing (a process in which pressurized fluid is forced into shale rock to free up oil or gas), have enabled the exploitation of difficult-to-extract deposits and allowed the United States to become a net petroleum exporter for the first time in decades.6 Employment in oil and gas industries has remained resilient even in the face of petroleum price declines in the second half of 2014.7

Nevertheless, in both oil and gas extraction and in support activities for oil and gas operations, job growth did slow somewhat in the last quarter of 2014. This slowdown perhaps reflects the fact that the newer techniques of domestic production are more costly than those used elsewhere in the world.8 The difference in cost suggests that, in many cases, break-even prices are higher for domestic than for foreign producers. As cheap oil flooded the global market in the last half of 2014, domestic producers began to curtail operations, a curtailment that led to slower employment growth in some cases and layoffs in others.9

The largest employment gain in 2014 came in the professional and business services industry, in which employment has been expanding for over 2 years. In 2014, the industry added 704,000 jobs—almost double the number of jobs lost in the 2007–2009 employment downturn—and, at the end of the year, was 8 percent above its most recent (December 2007) employment peak. Gains were about evenly split between professional and technical services (+299,000) and administrative and waste services (+350,000), the two largest broad component industries.

Employment gains in 2014 were widespread within professional and technical services, with computer systems design and related services adding the most workers over the year (+79,000). Establishments within this industry group provide expertise in information technology, both by catering to the software needs of clients and by planning or managing computer systems. Driven by the increased use and prevalence of information technology, employment in this industry has grown by well over 400 percent since 1990. Job gains in 2014 occurred primarily in computer systems design services (+40,000) and in custom computer programming services (+32,000).

Management and technical consulting services, another professional and technical services industry in which employment has more than quadrupled since 1990, added 74,000 workers to payrolls in 2014. Workers in this industry group are involved in providing a broad range of expert services to businesses and governments. As enterprises have become more complex, they have looked outside the organization for fresh perspectives and expertise not available internally.10 This practice has led to sustained job growth in management and technical consulting. Among the components of this industry, management consulting services saw the largest gain in 2014, adding 51,000 jobs.

Within administrative and waste services, the largest job gains came in employment services’ temporary help services component, which added 174,000 jobs in 2014. This component, which supplies temporary workers to firms, is often seen as an indicator of future economic growth. It tends to lead business cycle turning points, because firms dismiss temporary workers before permanent employees during downturns and hire temporary workers during early expansions, when economic improvement and demand are still tentative. For example, in 2010, when the U.S. economy was just emerging from recession, temporary help employment grew by just under 19 percent. Since then, however, annual growth has slowed to around 6 percent, perhaps indicating greater certainty about economic conditions.

Transportation and warehousing recovered from its most recent employment downturn in January 2014, and by the end of the year was 3.9 percent above its most recent employment peak, reached in April 2008. This industry added 166,000 jobs in 2014, with the largest gains coming from truck transportation, which added 47,000 jobs, and from couriers and messengers, which added 45,000 jobs. Both of these industries are extremely sensitive to the business cycle, with changing economic activity leading to a change in demand for their services.11

The evidence suggests that growth in e-commerce may have helped job growth in both truck transportation and couriers and messengers. Although the share of e-commerce in total revenue for these component industries was less than 1 percent in 1998, it had quickly grown to over 7 percent by 2013. As one illustration, figure 4 shows the increasing, albeit still small, percentage of trucking revenues from e-commerce.

In 2014, employment in other services also recovered from its recent losses. By the end of the year, it had exceeded its April 2008 peak by 71,000. Job gains in other services in 2014 were concentrated in personal and laundry services.

By the end of 2014, retail trade had recovered 94 percent of the jobs lost during its most recent employment downturn. Job gains in 2014 totaled 224,000. This total is well below retail trade’s employment gain experienced in 2013, as most component industries saw weaker growth in 2014. The largest employment gain occurred in motor vehicle and parts dealers (+67,000), and about two-thirds of that increase (+46,000) came from automobile dealers. Buoyed by a combination of low interest rates and an improving economy, motor vehicle sales have been improving steadily since 2009.12 Food and beverage stores also experienced strong job growth (+53,000) over the year, with that growth being concentrated in supermarket and other grocery stores, which added 41,000 jobs. Employment also rose in general merchandise stores (+46,000), with a gain in other general merchandise stores (+57,000) more than offsetting a small loss in department stores. Nonstore retailers,13 a retail component industry that has been growing steadily for several years, actually exceeded its 2013 performance, adding 34,000 jobs in 2014. The gain in this industry was concentrated in electronic shopping and electronic auctions, which added 26,000 workers in 2014. As shown in figure 5, since 2009, employment in nonstore retailers has paralleled e-commerce retail sales.

Wholesale trade has recovered almost three-quarters of the jobs lost during its most recent employment downturn. In 2014, employment in this industry grew by 114,000. The largest gain occurred in durable goods, which added 63,000 jobs. Over the year, nondurable goods added 35,000 jobs and electronic markets and agents and brokers added 16,000 jobs.

Although the financial activities industry ended 2014 below its employment peak of December 2006, it did add 135,000 jobs in 2014, marking a recovery of 52 percent. This employment gain was well above the 2013 gain of 88,000. Apart from credit intermediation and related activities,14 which experienced job losses in 2014, most component industries in financial activities recorded job gains that were larger than the previous year’s. The largest employment gains occurred in insurance carriers and related activities (+83,000) and in real estate and rental and leasing (+56,000).

The construction industry was among the hardest hit during the recession, losing nearly 2.3 million jobs between April 2006 and January 2011. By the end of 2014, the industry had regained only 37 percent of the jobs lost. Although the explanations for this slow recovery are many, a few stand out. As the economy faltered, home foreclosures increased and lending standards tightened, driving up the inventory of unsold homes.15 The result was a diminished demand for newly built homes. In addition, increasing unemployment and declining home values, which prevented homeowners from tapping a home’s value through “cash-out” refinancing, resulted in a decline in remodeling activity.16

Nevertheless, in 2014, the construction industry experienced its largest employment increase since 2005, adding 338,000 jobs, a gain of 5.7 percent. (See table 1.) Gains were widespread, with each of the three major component industries—construction of buildings, heavy and civil engineering construction, and specialty trade contractors—seeing faster job growth in 2014 than in 2013. Employment increases were concentrated in construction’s residential components, with residential specialty trade contractors experiencing the largest gain (+114,000). Residential building construction also saw a continued increase in employment (+49,000), with job gains in new single-family general contractors (+35,000) and residential remodelers (+10,000) accounting for virtually all of that increase. Job gains in residential construction align, to an extent, with residential construction-related indicators, such as building permit issuance, housing starts and completions, and construction expenditures. Although these indicators did not increase at the same rate as employment did, they do tell a story of sustained growth after the most recent recession.17

| Industry | Level changes (in thousands) | Percent changes | ||||||

|---|---|---|---|---|---|---|---|---|

| 2011 | 2012 | 2013 | 2014 | 2011 | 2012 | 2013 | 2014 | |

Construction | 145 | 112 | 213 | 338 | 2.7 | 2.0 | 3.7 | 5.7 |

Construction of buildings | 19 | 30 | 52 | 74 | 1.6 | 2.4 | 4.1 | 5.6 |

Residential building | 17 | 17 | 35 | 49 | 3.0 | 2.9 | 6.0 | 7.8 |

Nonresidential building | 2 | 13 | 17 | 26 | .4 | 2.0 | 2.5 | 3.8 |

Heavy and civil engineering construction | 34 | 19 | –1 | 56 | 4.2 | 2.2 | –.1 | 6.4 |

Specialty trade contractors | 91 | 64 | 161 | 208 | 2.7 | 1.8 | 4.5 | 5.6 |

Residential specialty trade contractors | 33 | 38 | 105 | 114 | 2.3 | 2.6 | 7.0 | 7.1 |

Nonresidential specialty trade contractors | 59 | 26 | 56 | 95 | 2.9 | 1.3 | 2.7 | 4.4 |

Source: U.S. Bureau of Labor Statistics, Current Employment Statistics survey. | ||||||||

Component industries in nonresidential construction also saw healthy employment gains in 2014. Nonresidential specialty trade contractors added 95,000 workers to payrolls, and nonresidential builders added 26,000 jobs, an increase that is largely due to an employment gain of 28,000 in commercial building. The job gain in commercial building corresponds to an increase in the value of commercial construction put in place, which has grown in each of the past 4 years.18 Heavy and civil engineering construction added 56,000 jobs over the year, a 6.4-percent increase that followed a decline of 0.1 percent in 2013. The employment increase in heavy and civil engineering construction, an industry largely dependent on public works projects, corresponds to an increase in the value of public construction expenditures, which has declined in each of the previous 4 years.19

Manufacturing has been losing jobs since the late 1970s. (See figure 6.) This trend may reflect long-term structural changes, which could be immune to overall economic recovery.20 These structural changes are well documented and include increases in labor productivity and the movement of labor-intensive manufacturing activity overseas, to low-wage countries. After the 2001 recession, the industry did not enter a period of employment recovery. Declines accelerated between August 2004 and March 2010, a period encompassing the most recent recession, with employment falling by 2.8 million. By the end of 2014, 29 percent of the jobs lost had been recovered. Job gains in 2014 totaled 215,000, the largest annual increase since 1997.

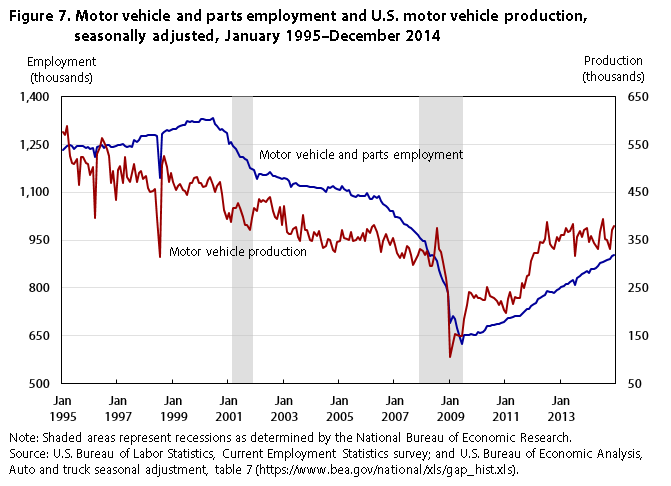

Gains were concentrated in durable goods manufacturing, which added 189,000 jobs in 2014. The largest job gain in durables came from transportation equipment (+60,000), in particular motor vehicles and parts (+50,000). This gain, the fifth consecutive annual increase, corresponds to gains in motor vehicle production and marks the resurgence of the motor vehicle and parts industry, which experienced dramatic employment declines during the most recent recession (see figure 7).21 Other durable goods industries that saw job growth in 2014 were fabricated metal products manufacturing (+31,000) and machinery manufacturing (+37,000). Employment growth in fabricated metals products is directly related to growth in both construction and transportation equipment, which are major users of the metal products the industry produces.22 In fact, the largest job gain within fabricated metals came from architectural and structural metals (+13,000). Job gains in machinery manufacturing—itself a significant purchaser of fabricated metal products—were also construction related and concentrated in agricultural, construction, and mining machinery manufacturing.

Employment in the information industry grew by 43,000 in 2014 and has recovered 26 percent of the 370,000 jobs lost between May 2007 and January 2012. This industry contains many component industries that have been adversely affected by the growth of the Internet. These include traditional publishing industries, such as book, newspaper, and periodical publishing—all of which have been in a long-term decline because of increased competition from their Internet equivalents. That traditional publishing is losing ground is illustrated by the fact that, among information component industries, the largest job gain (+22,000) in 2014 occurred in the Internet publishing and broadcasting and web search portals component of other information services. Traditional publishing, on the other hand, lost 8,000 jobs. While the information industry also includes industries such as data processing and website hosting, these industries have contributed little to job creation.

After several years of decline, government saw an employment increase of 74,000 in 2014. This increase came primarily from local government (+62,000), in particular local government education, which added 33,000 jobs over the year. However, the noneducation component of local government also made a turnaround in 2014, adding 29,000 jobs. State government experienced its largest over-the-year employment increase since 2008, adding 23,000 jobs, all of which came from the education component of the industry. Federal government employment continued to decline, losing 11,000 jobs over the year. By the end of 2014, the government sector had recovered only about 10 percent of the jobs lost during the 2007–2009 recession.

Education and health services did not lose jobs as a result of the most recent recession. In fact, except for a few isolated months of employment decline, this industry has experienced consistent job growth since the origination of the data series in 1990. The industry saw impressive growth in 2014, adding 488,000 jobs over the year—a growth rate of 2.3 percent. As is usually the case, this growth was concentrated in health care (+309,000). Long-term growth in the industry is largely driven by the increasing medical needs of the aging baby-boom generation.23 Health care employment growth in 2014 was concentrated in ambulatory health care services, which includes offices of physicians and outpatient care centers.

Educational services employment grew by 65,000 in 2014. This increase, the industry’s largest since 2011, was spread broadly across component industries. The largest gains occurred in the elementary and secondary schools component (+38,000), which more than doubled its 2013 job gain. Business, computer, and management training (+12,000) also saw a marked improvement over its 2013 employment performance.

As measured by CES data, the ongoing economic recovery marked a milestone in 2014, with both total private and total nonfarm employment entering an expansionary phase. About half of broad industry groups entered a period of job expansion, and others edged closer to recovery. Employment gains during the year were spread broadly across industries, and CES data on hours and real earnings indicate a stronger economy. Taken together with improvements in other prominent economic indicators, such as the unemployment rate,24 these gains have made 2014 a good year.

John P. Mullins and Brittney E. Forbes, "CES employment recovers in 2014," Monthly Labor Review, U.S. Bureau of Labor Statistics, April 2015, https://doi.org/10.21916/mlr.2015.10

1 The Current Employment Statistics (CES) program, which provides detailed industry data on employment, hours, and earnings of workers on nonfarm payrolls, is a monthly survey of about 143,000 businesses and government agencies, representing approximately 588,000 individual worksites. For more information on the program’s concepts and methodology, see “Technical notes to establishment survey data,” https://www.bls.gov/web/empsit/cestn.htm. To access CES data, see “Current Employment Statistics—CES (national),” https://www.bls.gov/ces. The CES data used in this article are seasonally adjusted unless otherwise noted.

2 John Coughlan, “Restaurants help feed job growth: how the leisure and hospitality industry fared after the recent employment downturn,” Beyond the Numbers, July 2014, https://www.bls.gov/opub/btn/volume-3/restaurants-help-feed-job-growth.htm.

3 Jonathan Maze, “Yes, gas prices are helping restaurants,” Nation’s Restaurant News, January 2015, http://nrn.com/blog/yes-gas-prices-are-helping-restaurants?NL=NRN-02_&cl=article_3&YM_RID=CPG06000000070364&YM_MID=1013.

4 Consumer Confidence Survey, The Conference Board, http://www.conference-board.org/data/consumerconfidence.cfm.

5 Maze, “Yes, gas prices are helping restaurants.”

6 Stephen P.A. Brown and Mine K. Yucel, “The shale gas and tight oil boom: U.S. states' economic gains and vulnerabilities” (Council on Foreign Relations Press, October 2013). See also Grant Smith, “U.S. seen as biggest oil producer after overtaking Saudi,” Bloomberg, July 2014, http://www.bloomberg.com/news/articles/2014-07-04/u-s-seen-as-biggest-oil-producer-after-overtaking-saudi.

7 According to the U.S. Energy Information Administration (www.eia.gov), the price per barrel of West Texas Intermediate crude oil fell from $105.79 in June 2014 to $59.29 in December 2014—a decline of 44 percent. Over the same period, the retail price of gasoline fell by 41 percent.

8 For a discussion of production costs, see Andy Tully, “Oil prices keep falling, but US drillers keep drilling,” The Christian Science Monitor, December 2014, http://www.csmonitor.com/Environment/Energy-Voices/2014/1210/Oil-prices-keep-falling-but-US-drillers-keep-drilling; and Roger Howard, “Is the U.S. fracking boom a bubble?” Newsweek, July 2014, http://www.newsweek.com/us-fracking-boom-bubble-258623.

9 John Kell, “Falling oil prices led to huge layoffs in January,” Fortune, February 2015, http://fortune.com/2015/02/05/job-cuts-soar-oil-price-drop/.

10 Chad Brooks, “Tech firms outsourcing more jobs than ever,” BusinessNewsDaily, March 2013.

11 Emily Richards and Frank Conlon, “Recession leads to lackluster employment in the trucking industry,” Issues in Labor Statistics, Summary 10–01 (U.S. Bureau of Labor Statistics, February 2010), https://www.bls.gov/opub/btn/archive/recession-leads-to-lackluster-employment-in-the-trucking-industry.pdf. See also “Industry analysis: trucking,” Value Line, https://www.valueline.com/Stocks/Industries/Industry_Analysis__Trucking.aspx.

12 Auto and truck seasonal adjustment, table 6 (U.S. Bureau of Economic Analysis, March 2015), https://apps.bea.gov/national/xls/gap_hist.xlsx.

13 Establishments in this subsector include mail-order houses, vending machine operators, home delivery sales, door-to-door sales, party plan sales, electronic shopping, and sales through portable stalls (e.g., street vendors, except food).

14 The credit intermediation and related activities subsector includes establishments that (1) lend funds raised from depositors, (2) lend funds raised from credit market borrowing, or (3) facilitate the lending of funds or issuance of credit by engaging in such activities as mortgage and loan brokerage.

15 The unsold homes inventory, measured by the U.S. Census Bureau as the projected inventory-clearing number of months of supply of new homes, fell to a historic low of 3.5 months in June 2003; by January 2009, it had risen to 12.2 months (https://www.census.gov/construction/nrs/pdf/fsalmon.pdf).

16 Robert Dietz, “The importance of home equity loans for remodeling” (National Association of Home Builders, Eye on Housing, December 2011). See also the Joint Center for Housing Studies’ Leading Indicator of Remodeling Activity (Harvard University) (http://www.jchs.harvard.edu/sites/jchs.harvard.edu/files/lira_historical_data_2014_q4.xlsx) and the National Association of Homebuilders’ Remodeling Market Index (http://www.nahb.org/).

17 “Guide to data sources for construction from the U.S. Census Bureau” (U.S. Census Bureau), https://www.census.gov/econ/construction.html.

18 Ibid.

19 The value of total public construction put in place, as measured by the U.S. Census Bureau, increased by 1.6 percent in 2014, after declines of between 2.8 and 5.4 percent from 2010 to 2013 (https://research.stlouisfed.org/fred2/series/TLPBLCONS/downloaddata).

20 Megan M. Barker, “Manufacturing employment hard hit during the 2007–09 recession,” Monthly Labor Review, April 2011, https://www.bls.gov/opub/mlr/2011/04/art5full.pdf.

21 Auto and truck seasonal adjustment, table 7 (U.S. Bureau of Economic Analysis, March 2015), https://apps.bea.gov/national/xls/gap_hist.xlsx.

22 Data on the inter-industry use of commodities are from input–output accounts of the U.S. Bureau of Economic Analysis (https://apps.bea.gov/iTable/index_industry_io.cfm).

23 “How baby boomers consume health care [infographic]” (Concordia University, March 2013), http://online.csp.edu/blog/healthcare/how-baby-boomers-consume-health-care-infographic; and “How the baby boomer generation is changing the U.S. healthcare system,” Huffington Post, August 2013, http://www.huffingtonpost.com/visualnewscom/us-health-care-how-the-baby-boomer_b_3369175.html.

24 Eleni Theodossiou Sherman and Janie-Lynn Kang, “Continued improvement in U.S. labor market in 2014,” Monthly Labor Review, April 2015, https://www.bls.gov/opub/mlr/2015/article/continued-improvement-in-u-s-labor-market-in-2014.htm.